Stakeholder theory – first proposed in 1984 by R. Edward Freeman – stresses that because of their interconnectedness, businesses must be aware of and make decisions deemed ethical by a variety of constituents. Most agree that stakeholders can be grouped into six categories – community (M), customers (C), employees (E), investors (I), suppliers (S) and more recently, the environment (V) – which, despite its importance, I’ll set aside because of the absence of people.

Let’s assume that all individuals within each of these groups were united by a singular purpose. For example, shareholder agreed on a minimum acceptable return on investment. Together, the community established ethical standards which all organizations within the community must follow. Or employees agreed on their collective expectations – fair compensation, an opportunity to participate and be valued for their contribution.

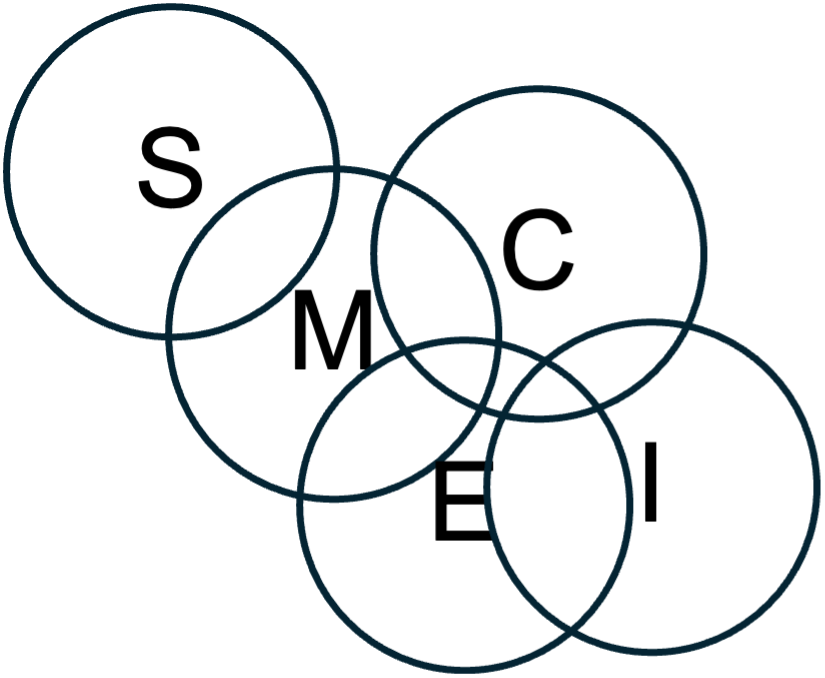

These five groups – each united by a singular purpose – could be represented as follows:

While there might be some common need or interest amongst the different groups – for example, the longevity of the business – those interests aren’t 100% identical. For example, some stakeholders are more severly impacted by a business failure than others. This connectivity, as represented below, shows there is some, but not complete overlap.

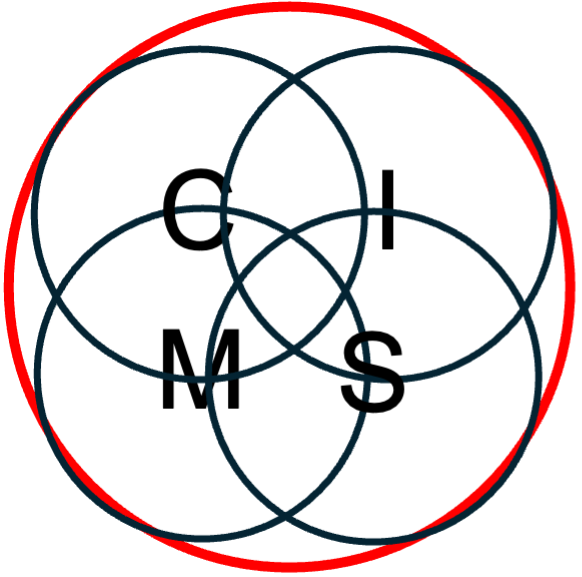

As the interests of each stakeholder converge, there is greater overlap and a singular overarching purpose starts to emerge.

When it does, I call this the Sweet Spot.